|

| horizontal vs vertical credit intermediation |

In April, European officials

finally realised that Europe's banks will be unable to lend enough to small businesses to finance economic recovery. The

failure of the UK's Funding for Lending scheme has not gone unnoticed. So rather than establish an EU version of that scheme, the European Central Bank has been

considering whether to kick-start a small business securitisation market. Last week, however, the ECB

played down that idea. After all, the banks don't have the capability to make enough loans in the first place, and the

'shadow banking' sector has demonstrated that it can't

reliably price endless tiers of bonds, CDOs, CDOs of CDOs.

So now what?

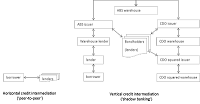

Peer-to-peer lending has grown rapidly in the UK, despite an awkward (though permissive) regulatory framework and

perverse tax incentives. That headwind is changing, as

even the UK government has begun lending on some platforms, and officials are getting on with the job of

bringing P2P lending firmly within the regulatory sphere.

Oddly, perhaps, those regulatory changes are being made in the context of moving the supervision of consumer credit from the Office of Fair Trading to the Financial Conduct Authority in April 2014. However, that merely reflects the fact that P2P lending originated in the personal loan market, whereas there are now platforms that facilitate business loans, asset finance and commercial real estate funding. In other words, P2P lending has expanded into institutional investor territory, which should be of real interest to the ECB as it looks beyond the banking sphere.

As I've pointed out many times

since 2010, a key feature of P2P lending platforms is that each borrower's loan amount is provided via many tiny, direct loans from many different lenders at inception. This permits lenders to diversify at the outset, so that loan maturities and rates of return do not need to

be 'transformed' via securitisation later on. Enforcement and due diligence are made easy on P2P platforms because the one-to-one legal

relationship between borrower and lender is maintained for

the life of the loan, and the performance data also remains readily available via the lender's account. This enables P2P lenders to avoid the concentration of credit risk that securitisation tends to obscure through endless re-packaging

and re-grading, and the ensuing disconnect between bonds and the underlying loans.

It will also be of special interest to the ECB that the scope for moral hazard is contained in the P2P context - the platform operator itself has no balance sheet risk, yet is able to implement all the compliance and operational risk controls one would ordinarily expect of lenders. This brings regulatory efficiencies, too. The authorities need only supervise the P2P platform operator rather than the lenders and borrowers on either side, who are effectively just payers and payees, as in the case of a payment institution. Funnily enough, that's the reason the UK's Peer-to-Peer Finance Association borrowed the substance of its "

Operating Principles" from the Payment Services Directive - a piece of legislation with which the ECB is also very familiar...

That paves the way for anyone to lend to consumers and small businesses via P2P platforms without any concern about the need for lender-licensing. Indeed, the UK's Financial Conduct Authority has

said that it intends providing investor-type protection for P2P lenders. That would mean exemptions for marketing P2P lending to high net worth and sophisticated investors and professional investment firms. So it would be strange to also require such investors to be separately authorised to lend, especially when the platform operator is taking care of all the compliance obligations. It would be like requiring a firm to be authorised to deposit money in the bank or to make payments via a payment institution - just red tape.

Given access to loan capital on that industrial scale, the ECB could justifiably view P2P lending to small businesses as a significant potential driver of economic growth.